7 July 2026

SOURCE: CPF Board

MediShield is a health insurance scheme designed to help Singaporeans cope with large hospital bills and selected costly outpatient treatments. It aims to make healthcare more affordable and accessible to all, regardless of age or health conditions and covers all Singaporeans and Permanent Residents (PRs).

But what does MediShield Life cover exactly? Learn about the components of a hospital bill and what you can claim:

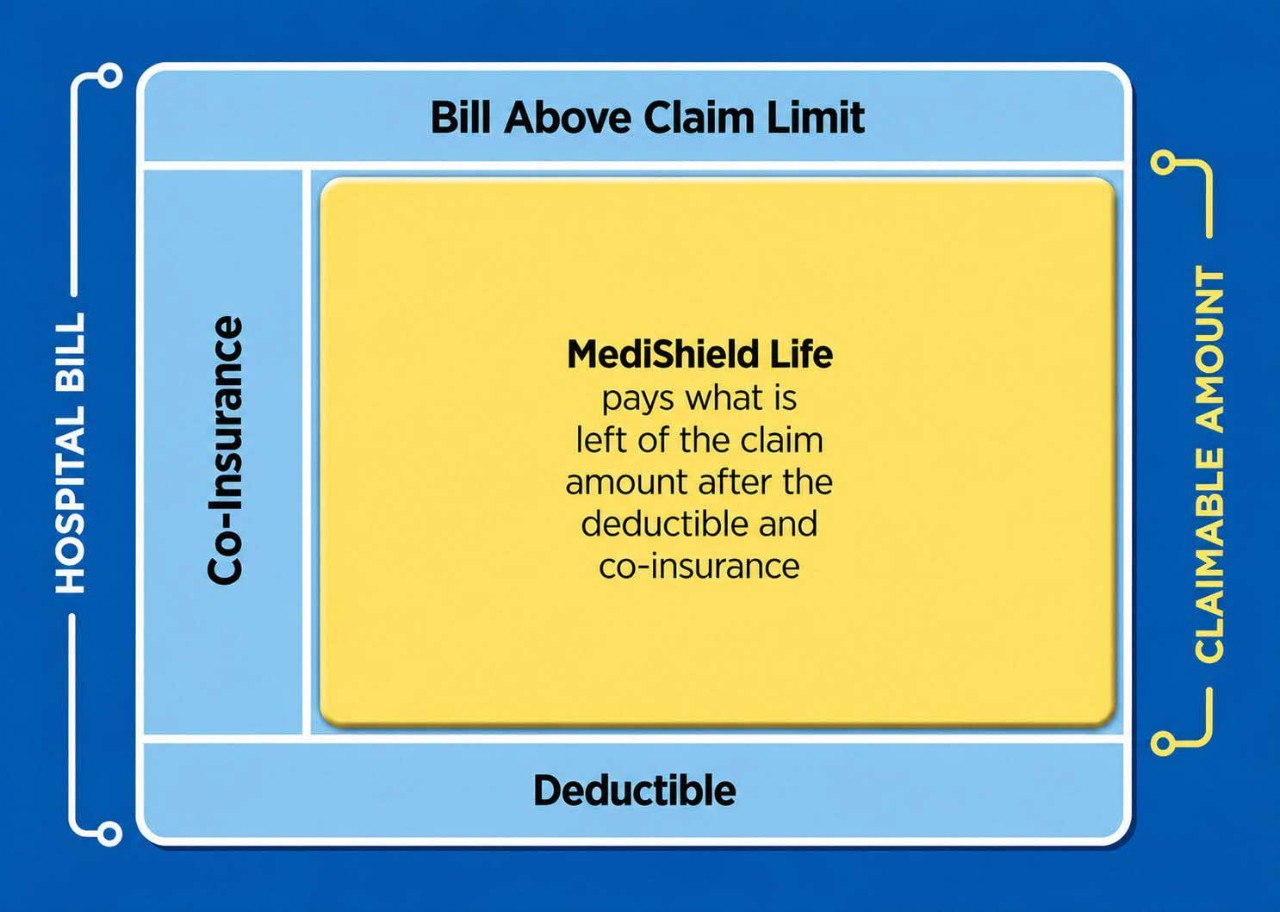

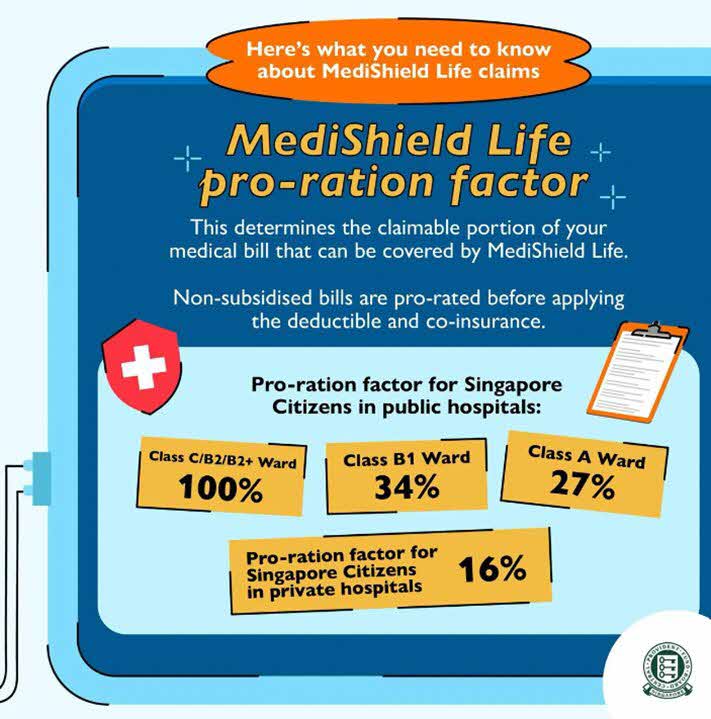

MediShield Life does not cover the entirety of the bill. The claimable amount for a bill is determined by adjusting the bill based on the pro-ration factor and applying the claim limits.

MediShield Life provides the highest level of coverage for subsidised treatment in Class B2/C wards and subsidised outpatient treatments or day surgeries at public hospitals. If you choose higher ward classes or other non-subsidised treatment options, a smaller portion of your bill may be claimable as the bill will first be adjusted using a pro-ration factor before claim limits are applied.

How much you can claim depends on the type of treatment you receive, and the length of your hospital stay. The maximum claim limit per policy year is $200,000 with no lifetime limit on the amount you can claim from MediShield Life. You will have to pay the portion the bill that is above the claim limit.

Learn the MediShield Life claim limits for the different categories of benefits.

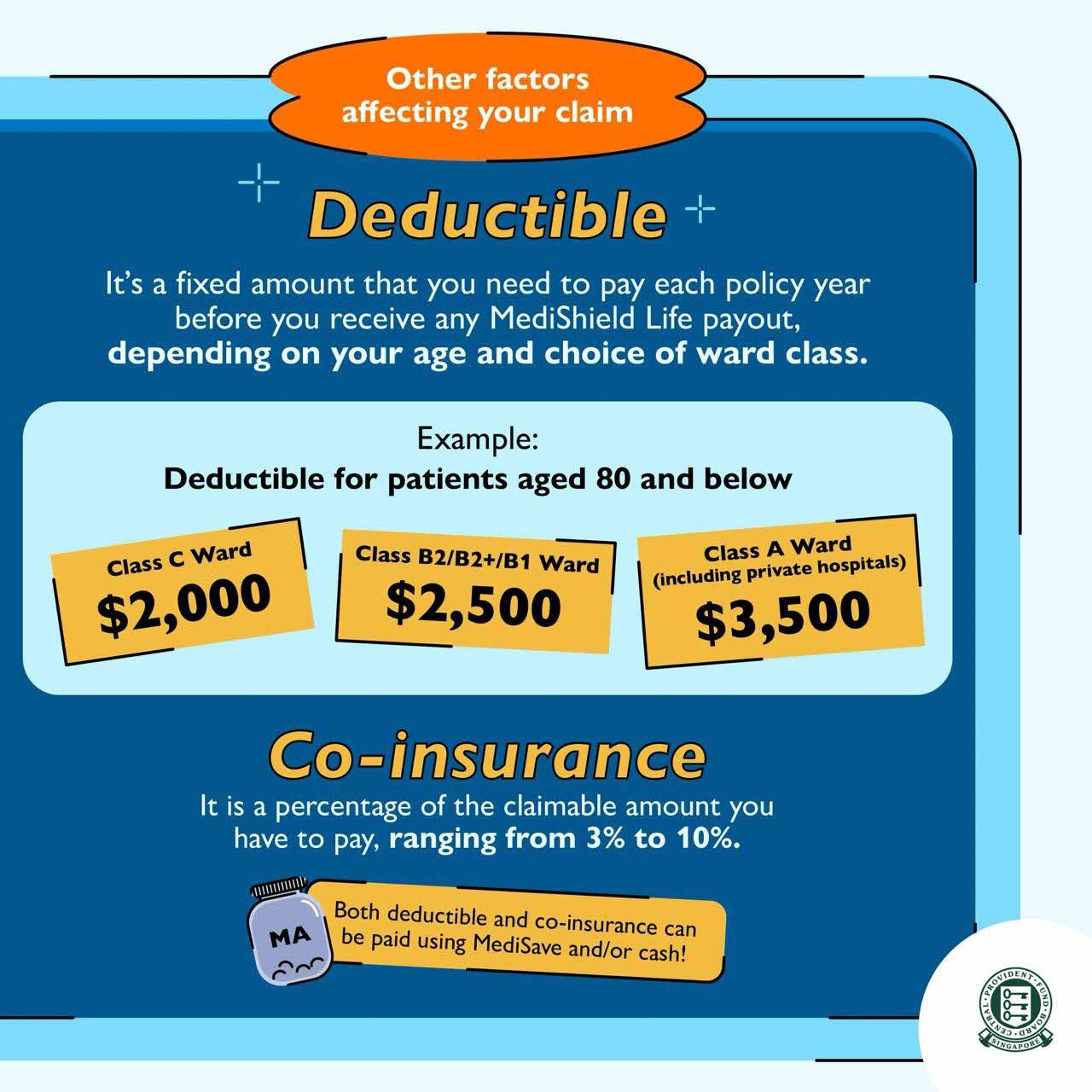

This is the fixed amount you have to pay before your MediShield Life payout kicks in. The deductible ranges from $500 to $3,000, depending on your age and choice of ward class.

The deductible is applied once each policy year, regardless of the number of claims you make during that period. It is typically deducted from your hospital bill at the point of claim and can be paid using your MediSave savings and/or cash.

Having a deductible helps keep MediShield Life premiums affordable for everyone by ensuring that policyholders share a portion of their healthcare costs, especially for smaller claims.

This is a percentage of the claimable amount that you must pay after the deductible. The co-insurance rate decreases from 10% to 5% and then 3% as the claim amount increases. Like the deductible, the co-insurance is deducted as part of your hospital bill and can also be paid using your MediSave savings and/or cash.

MediShield Life will cover the portion of your medical bill after you pay the deductible and co-insurance.

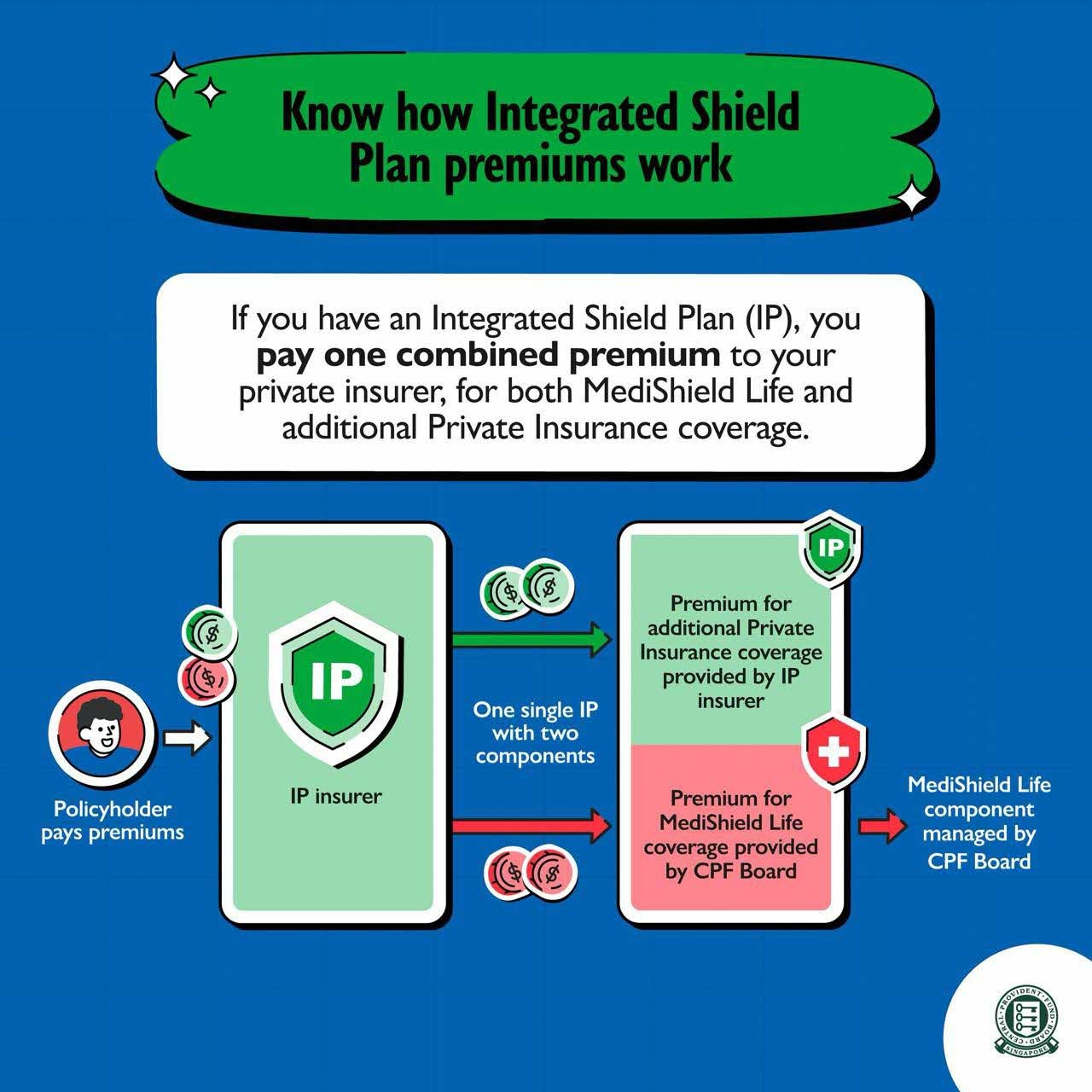

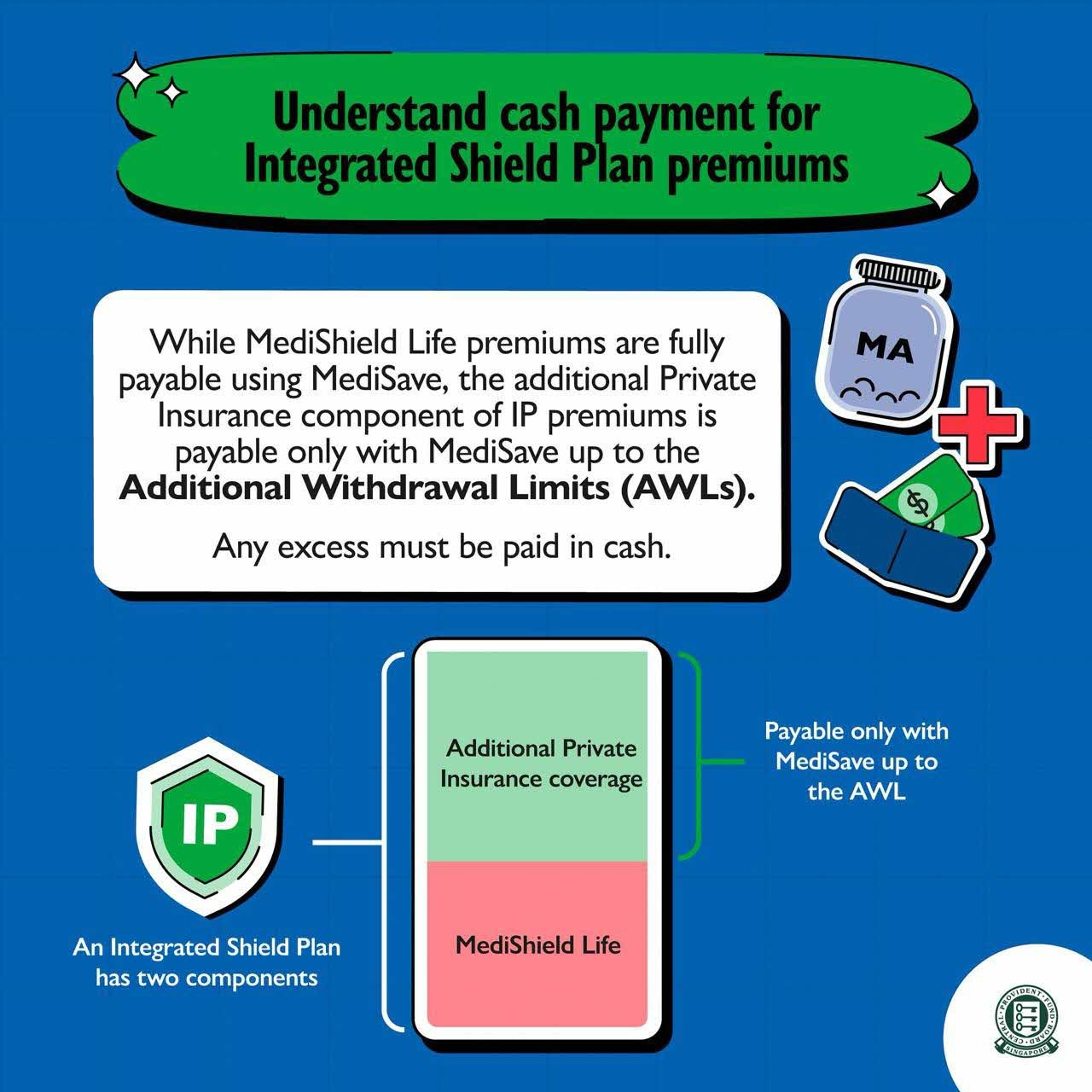

An IP comprises two parts: the MediShield Life component and an additional private insurance coverage component offered by a private insurer.

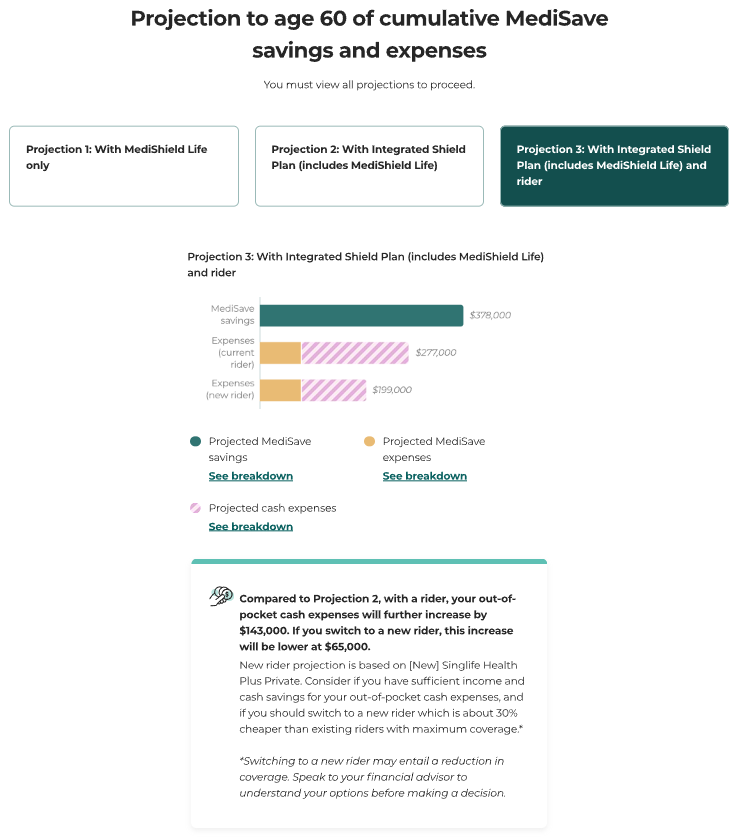

Not sure whether to keep your current legacy IP rider or switch to a new IP rider?

The CPF Health Insurance Planner (HIP) can help you compare your choices. It now includes the new IP riders, allowing you to see how different options may affect your premiums and out-of-pocket costs.

Where your legacy rider premiums exceed those of a comparable new rider, the planner will highlight this for you. With a side-by-side comparison, you can gain a clearer picture of your long-term out-of-pocket costs and make a more informed decision on whether the cost of your current rider remains sustainable over time. As switching riders may involve a reduction in coverage, you should speak to your financial advisor before making any decision.

To utilise MediShield Life or an IP to pay for your medical expenses, you can inform the staff responsible for your admission or outpatient treatment. They will handle the claim submission on your behalf. CPF Board or the private insurer (if you have an IP) will process your claim and directly settle the payment with the medical institution.

To better understand how MediShield Life claims work, let’s take a look at Daniel, a 35-year-old Singapore Citizen who underwent a gallbladder removal surgery and was hospitalised in a public hospital C ward for five days. His total bill came up to $12,500.

After government subsidies, Daniel's hospital bill payable was $4,000. As he is a Singapore Citizen who stayed in a subsidised C ward, no pro-ration applies to his MediShield Life claim. As the daily ward and treatment charges, as well as the operation charges, are within the applicable MediShield Life claim limits, Daniel's total claimable amount is $4,000.

As Daniel is under 80 years old, there is a deductible of $2,000 for his stay in a C ward in a public hospital. A co-insurance component also applies.

|

MediShield Life Claim Computation |

Total claimable amount |

$4,000 |

Deductible |

($2,000) |

Claimable (less deductible) |

$2,000 |

Co-insurance (10%) * |

($200) |

MediShield Life payout |

$1,800 |

Daniel’s out-of-pocket payment |

$2,200 |

*Co-insurance is 10% because the remaining claimable amount falls within the first $5,000 tier.

To compare legacy versus new riders, let’s say Daniel instead chooses to be treated as a patient at a private hospital for the same surgery. His total bill comes up to $26,347.

Without any rider (IP only)

|

Amount |

Total bill |

$26,437 |

IP Deductible |

($3,500) |

Claimable (less deductible) |

$22,937 |

Co-insurance (10%) * |

($2,294) |

Daniel’s out-of-pocket payment |

$5,794 |

With a rider

|

Legacy rider |

New rider |

IP Deductible |

$3,500 |

$3,500 |

Covered by rider |

($3,500) |

($0) |

Co-insurance (5% of balance, panel/pre-authorised) |

$1,147 |

$1,147 |

Covered by rider |

($1,147) capped at $3,000 per year |

($1,147) capped at $6,000 per year |

Daniel’s out-of-pocket payment |

$0 |

$3,500 |

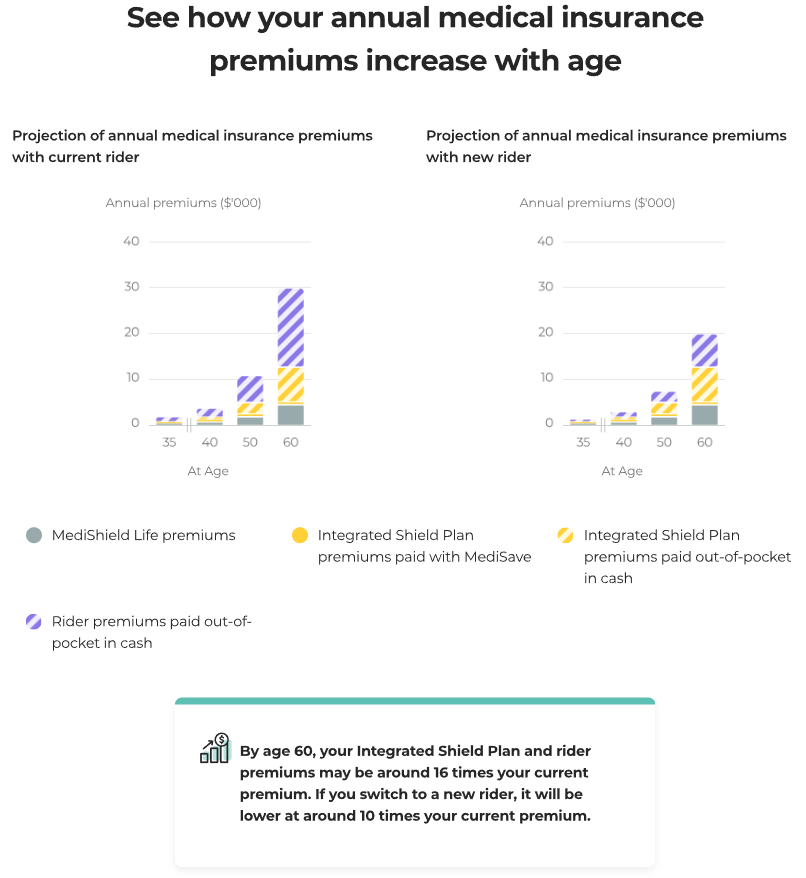

The right choice depends on your healthcare preferences, your financial plan and how premiums will rise as you age. It’s worth reviewing this with the HIP, rather than assuming more coverage is always better.

The information provided in this article is accurate as of the date of publication.

_600x400.webp/jcr:content/renditions/cq5dam.thumbnail.300.200.webp)