30 May 2025

SOURCE: CPF Board

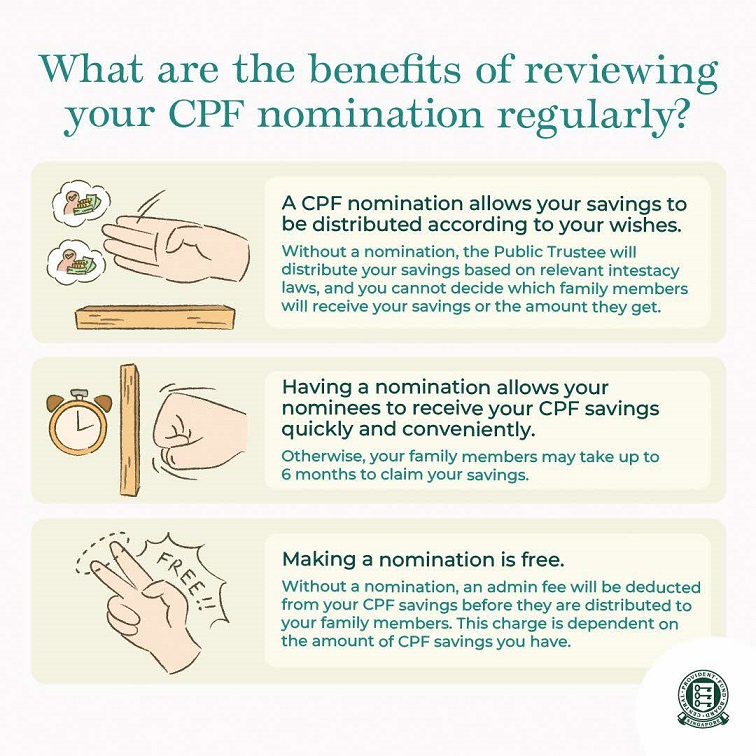

Life is full of uncertainties, but one thing you can control is how your CPF savings will be distributed after you're gone. A CPF nomination ensures your hard-earned savings reach your loved ones swiftly and according to your wishes, without any cost or lengthy legal processes.

Think of a CPF nomination as your final act of care towards your loved ones - one that requires careful thought and regular review. Just as your life circumstances change over time, your nomination should evolve to reflect your current intentions and family situation.

Many people make a nomination and forget about it, but life's milestones like marriage, having children, or changes in family relationships might mean your previous nomination no longer reflects your wishes. That's why it's important to review your nomination at least once a year or after significant life events.

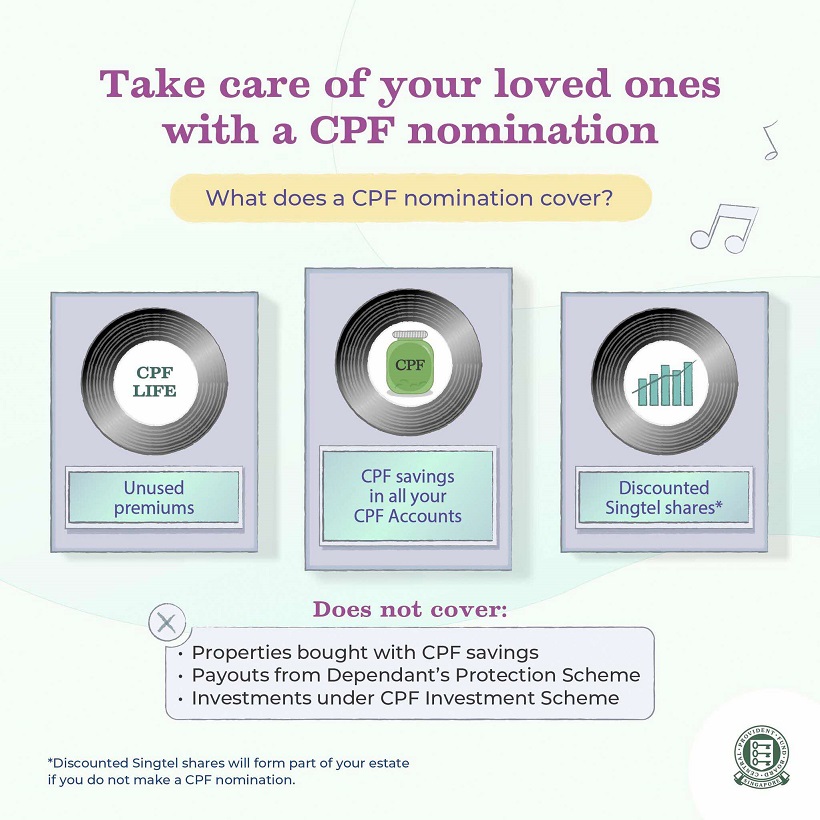

Your CPF nomination covers all savings across your CPF accounts — the Ordinary Account (OA), Special Account (SA), Retirement Account (RA), and MediSave Account (MA). It's important to note that these CPF savings do not form your estate and cannot be controlled by your will, and this protects your CPF savings from creditor claims for outstanding debts, allowing your beneficiaries to receive your savings in full.

If you're enrolled in CPF LIFE (automatic inclusion for Singapore Citizens and Permanent Residents born in 1958 or after with at least $60,000 in retirement savings before age 65), any remaining premium balance at the time of your passing will be distributed according to your nomination.

For members who purchased discounted Singtel shares through the Special Discounted Shares (SDS) Scheme in 1993 (ST "A" shares) or 1996 (ST2 shares), these shares are included in your CPF nomination.

Any properties bought using your CPF savings fall outside the scope of CPF nomination. These assets need will be handled separately based on how you own them.

If your property is held under:

- Sole ownership: forms part of your estate and will be distributed according to your will

- Joint Tenancy: ownership of property will be transferred to the surviving owner(s) without a need for a will

- Tenancy-in-Common: your share of the property goes to your estate and will be distributed according to your will

Note: If you have not left a will upon your passing, your estate will be distributed according to the relevant intestacy laws or inheritance certificate (for Muslims).

While the DPS is a term life insurance scheme that provides basic financial protection for you and your family, its payouts are not part of your CPF nomination. You should make a DPS nomination form to specify how you want to distribute the DPS payouts.

Your CPFIS investments* and any cash balance in your Investment Account will form part of your estate upon your passing. This allows the beneficiaries of your estate to decide how best to manage these assets, including the preferred timing for the sale of assets such as unit trusts and stocks.

* Except for insurance policies where the member had made an insurance nomination with the respective insurance company. The nominated beneficiaries can contact the insurance company to claim the death benefits.

Life changes, and your CPF nomination might too. It should be part of your regular financial review, particularly after significant life events such as:

- Marriage1 or divorce

- Birth of children

- Death of nominated beneficiaries2

- Significant changes in family relationships

1 Your existing nomination will be revoked upon marriage

2 A deceased nominee’s share will be reallocated to the surviving nominee(s)

By understanding what your CPF nomination covers and doesn't cover, you can better plan for your legacy and ensure your loved ones are properly provided for. Consider reviewing your nomination today - it's a simple step that can make a significant difference in your family's future financial security.

Information in this article is accurate as at the date of publication.