5 Aug 2025

SOURCE: CPF Board

Do you remember what it was like in primary school when you had to make do with $1.50 of pocket money? You probably didn’t realise it at the time but Mum’s quiet discipline, encouraging you to save those extra 30 cents left from buying a bowl of noodles instead of spending it all on a random item from the bookshop only to be forgotten the next day, was her way of teaching you to spend only on what you needed, so you can save the rest.

Looking back, what Mum was really teaching us wasn’t how to get by with less. It was how to pause, consider our needs, and make deliberate choices rather than impulsive ones. It was never just about frugality, but about intention. That’s a lesson that still holds today. In a world where it’s easy to let other people’s lives set the standard, real financial maturity means taking responsibility and abiding by your own habits, no matter how unglamorous and mundane they might seem.

It means knowing when to say no to the sale you don’t need, the new phone that looks sleek but adds little value, or choosing the $1.50 kopi today because you already had that $7 latte yesterday. It’s recognising that being in control of your finances such as building savings, getting closer to your goals, making CPF top-ups, means having the confidence to stay on track toward your goals, and the resilience to weather life’s unexpected setbacks.

Fast forward to today, it’s normal to justify spending, such as upgrading your phone when the current one still works fine, booking a cab instead of taking public transportation. You tell yourself, You’ve earned it. But behind each scenic holiday selfie or post-renovation home photoshoot, there’s often quiet financial strain at times. Remember Sofia? On paper, she had it all: dream apartment, weekend getaways, a wardrobe to envy. But privately, she admitted she was just one unexpected bill away from panic. It’s not freedom if you’re spending just to keep up.

You would agree that you made the right decision to automate saving each payday, steadily growing your savings account and CPF Special Account. Remember when you first set it up after a few years of working? You weren't even sure if it was worth it. Saving $50 a month didn't seem... significant? But every six months, you checked your progress and saw your savings grow steadily. Every time you refreshed your CPF balance, it felt like a tiny victory, and gave reassurance that you were on the right track.

And at the start of each year, when the interest is credited to your CPF accounts, that feels like an even bigger win! Let’s also not forget the benefit of paying less tax, and with an annual return of 5% p.a.*, how your $50 saved every month in your Special Account will grow to about $39,860 in 30 years. That’s better than the $18,000 you would have if you did nothing with it!

*Based on the current 4% p.a. interest rate floor on Special, MediSave and Retirement Account monies.

Remember your first job, how you budgeted just enough for bills and basic meals, and how your definition of a comfortable life was simply having enough for a café meal once a week? Then you progressed; your income rose and your goals shifted. Now that you’re married with a family, comfort means splurging on a nice dinner every once in a while, and going on family trips.

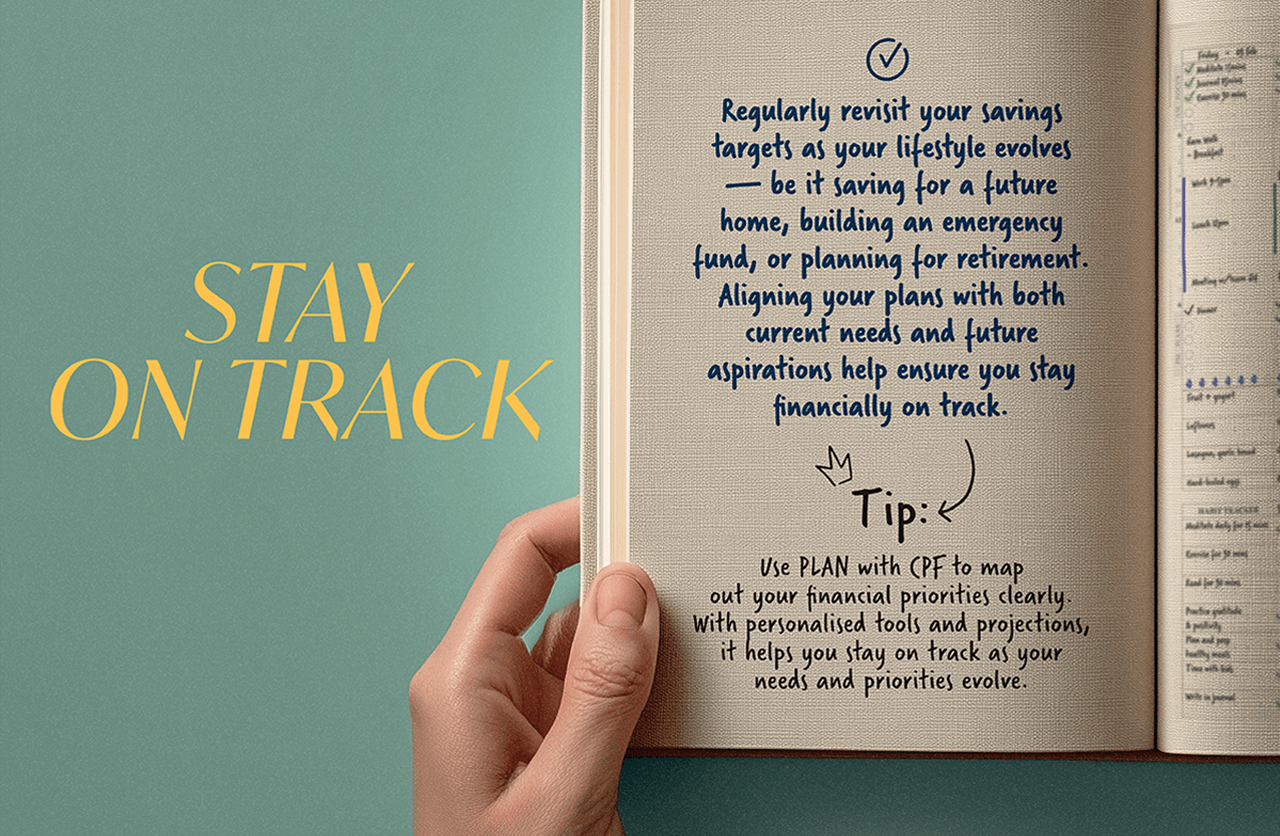

If you think about where you are now, it’s easy to see how important reviewing your saving goals and being intentional about lifestyle choices are. It's crucial to keep your spending habits in check for your savings to continue growing as your lifestyle evolves. Looking ahead, if you feel like you’re faltering, motivate yourself by tracking the following:

- How much your savings have grown;

- How your financial goals are still aligned with what matters most to you; and

- How your savings will grow.

You can do all this with tools such as the Retirement Payout Planner.

Remember all the discussions you had with your friends about how to get your money to work harder? Jim was losing sleep, obsessing over day-trading and chasing quick gains. But Jody had a different approach, such as growing her savings steadily by investing in low risk products like Singapore Savings Bonds (SSBs). There are different strokes (and risk appetites) for different folks, but there’s something reassuring about Jody’s steady approach.

Placing your emergency savings in options like Singapore Savings Bonds offers stability and flexibility, allowing you to redeem them any month if needed. For longer-term savings you don’t need to touch soon, Treasury Bills and fixed deposits can also offer peace of mind and stable growth.

No matter how far you’ve come, never lose sight of this: staying true to yourself and committed to your savings goals.

There will always be someone who seems to have more. But what they have doesn't change what you’ve built. Success isn't defined by Instagram likes or by matching someone else’s spending habits. It’s defined by security, independence and the confidence that comes from knowing you're financially prepared for the life you want.

Please never stop practising those seemingly mundane but incredibly empowering financial habits. Keep automating those CPF top-ups, growing your savings, and never lose sight of your long-term goals.

You’ve already learned the hardest lesson: financial peace is powerful. It gives you the freedom to rest easy, knowing your future is accounted for, your goals are within reach, and your retirement is well on track.

Keep up your savings habit by making a cash top-up today. Enjoy steady compounding interest, earn tax relief, and give yourself confidence for the future. Because the real win? Living confidently and meaningfully, on your own terms.

Your Younger Self

Information in this article is accurate as at the date of publication.