4 Nov 2022

SOURCE: CPF Board

Take a leaf from Iskandar and Alyssa to see how you can plan your finances to build a loving home and a meaningful retirement for yourself and your loved ones.

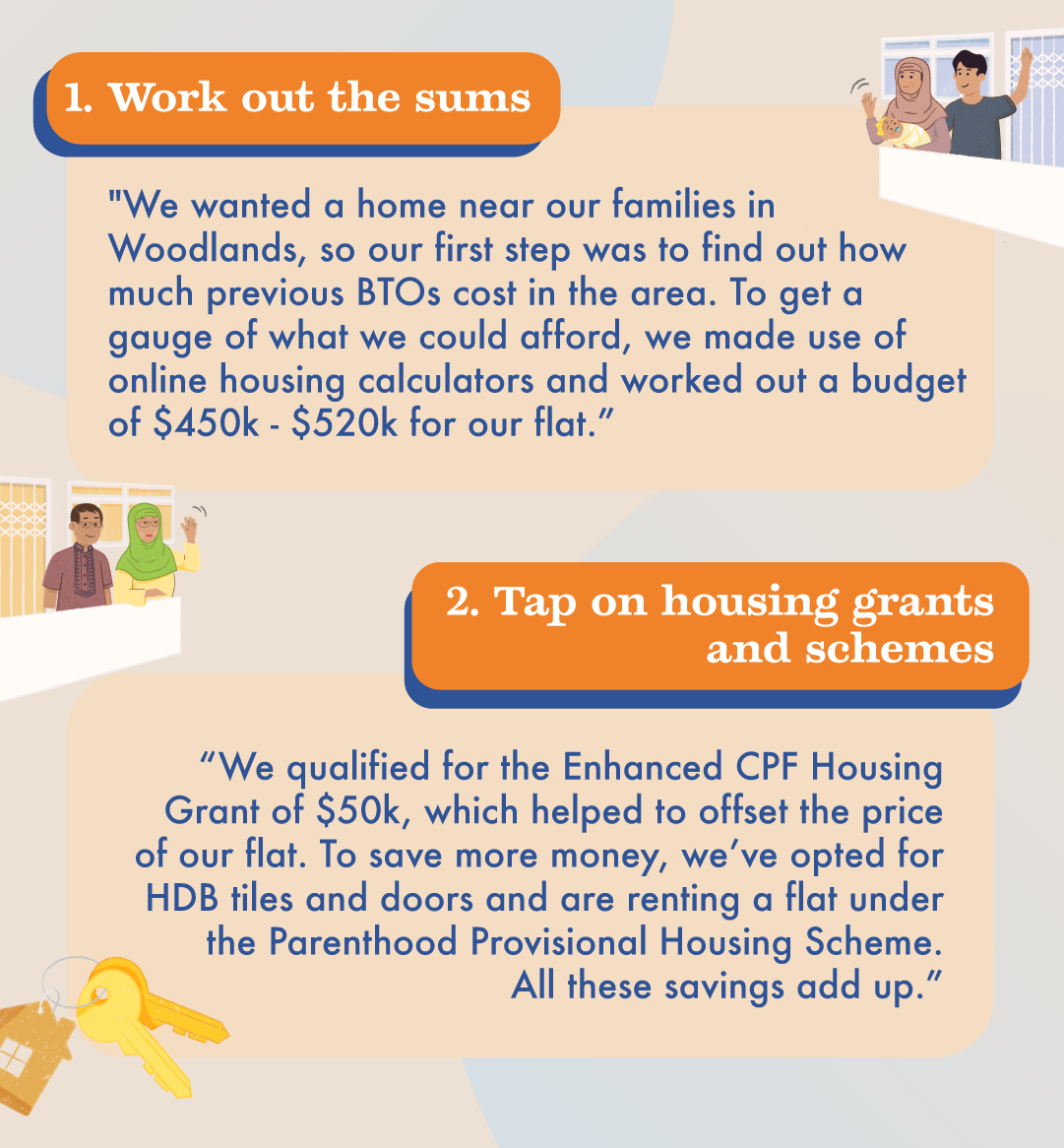

1. Work out the sums

As Iskandar and Alyssa wanted to stay in Woodlands to be close to their families, the first thing they did was to research on the previous BTOs prices in that area and set a budget for their home based on their combined income and CPF savings.

Online resources such as articles and financial tools were useful to the couple. “As potential homeowners, it’s important to be proactive and take initiative to do research,” Alyssa says. "Though it might not always be relevant to your situation, just having a rough gauge would be useful.”

Naturally, the couple understood that some small sacrifices needed to be made to save up for their dream home. They bit the bullet, and cut down on big purchases and long holidays. However, they still continued to pursue other hobbies such as rock climbing and handicrafts for some meaningful time together.

2. Tap on housing grants and schemes

When they finally got their BTO on their fifth try, Iskandar had worked for just over a year and a half, while Alyssa had just returned to work after completing her studies. “Previously, I’d question why part of my salary needs to go to my CPF,” Alyssa says. “But after making our downpayment, I see the purpose behind it. We wouldn’t have been able to afford our flat if not for the monies in our CPF."

The couple also looked for ways to save costs. “We applied for housing grants and got the Enhanced CPF Housing Grant which gave us $50,000,” Iskandar shares. “We also opted for tiles and doors from HDB directly, as they were cheaper.”

"As our BTO will only be ready in 2026, instead of renting a place in the open market, we applied for a rental flat under the HDB Parenthood Provisional Housing Scheme. It allows those waiting for their BTOs to rent a place at a more affordable rate. This helps us a lot with saving up for our eventual home and we still get to spend quality time together as a family with our newborn.”

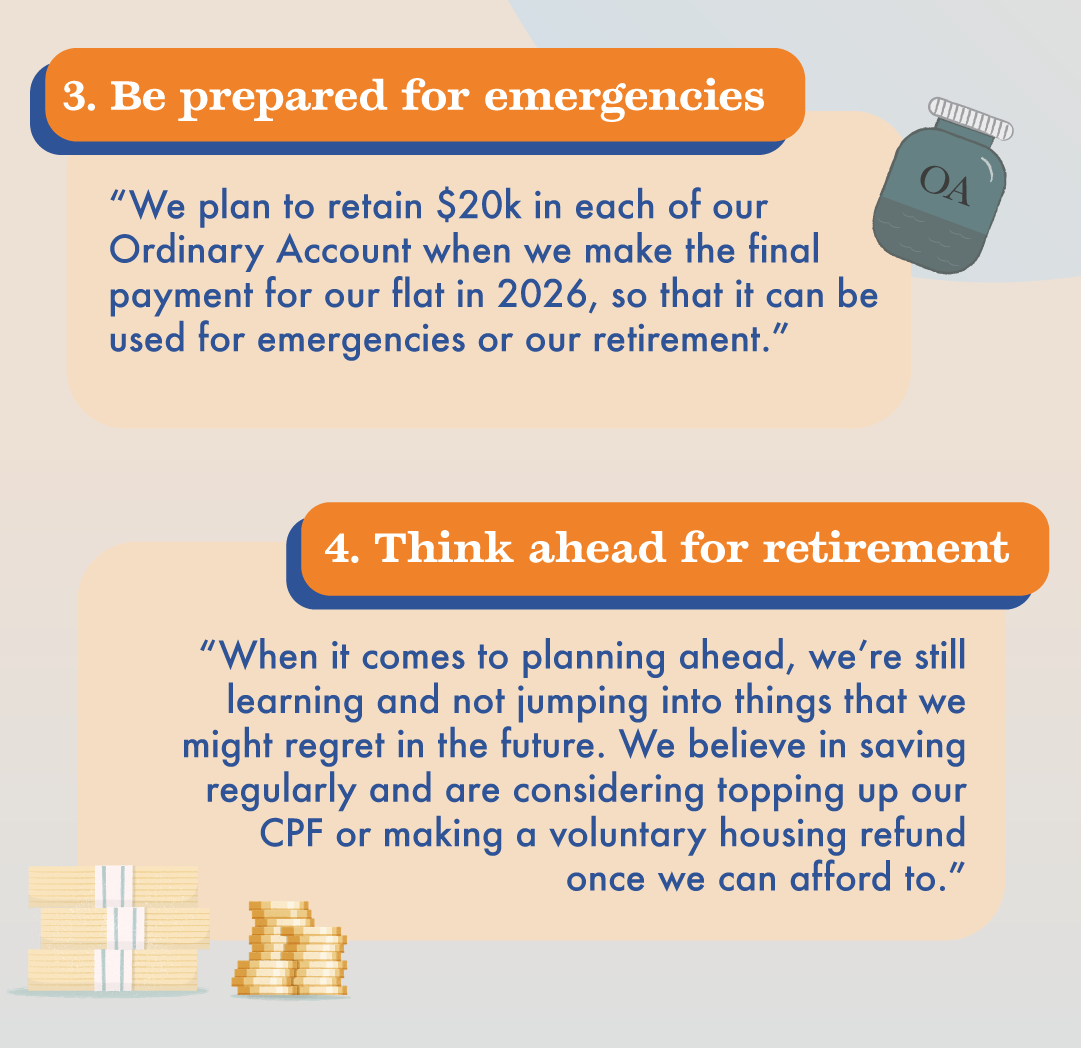

3. Be prepared and think ahead

Iskandar and Alyssa were able to comfortably pay the 5% downpayment for their BTO using their CPF. When the time comes for them to make the next payment when they receive their keys, they’re planning to retain $20,000 in each of their Ordinary Account to grow at a safe and stable interest rate of up to 3.5% p.a. for their retirement. “Once we’re ready to take the next step with our finances, we’re looking at making top-ups to our CPF or voluntary housing refund, so that we’ll have more savings for our retirement,” Iskandar says.

In addition, Iskandar & Alyssa can rest assured that their home is protected with the Home Protection Scheme (HPS). HPS is a mortgage-reducing insurance which protects against losing your HDB flat in the event of death, terminal illness, or total permanent disability.

“This home-buying process has been a journey through which we’ve learnt so much, not just about finances but also about ourselves,” Iskandar says. “We were discouraged numerous times whenever we were notified that we couldn't get the BTOs we applied for, but the ups and downs taught us to trust the process, support each other, and keep communication open. That's why financial planning is so important — it gave us the reassurance and confidence we needed to keep us going with our plan to build a home for life together."

Information in this article is accurate as at the date of publication.