14 Oct 2022

SOURCE: CPF Board

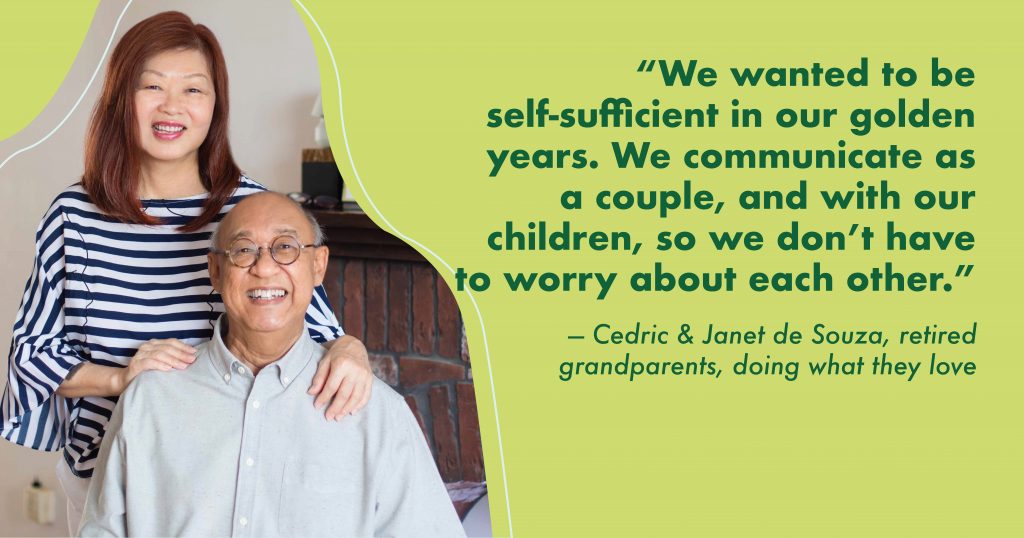

My name is Cedric. I spent many years in advertising before retiring from the industry, and I’m currently a freelance educational consultant. Janet, my wife, used to be a bank officer and is now running her own home bakery from our HDB flat in Pasir Ris. We’ve been married for 43 years and have two children — our older son is based in Perth, while our daughter works in a bank in Singapore. We’re also blessed with two grandchildren, with one more on the way!

This sounds like your run-of-the-mill setting of familial bliss. But if I reflected on how I managed all of that and am comfortably semi-retired today doing what I love — I must admit that there was initially little planning on our part, so we got lucky in some ways.

Struggled with our finances stretched to its limits

Back then our wages were just sufficient to cover our monthly expenses and we thought that was a statement of comfort. We felt fine getting by every month like that. But it wasn’t until we had our first child that we had a rude awakening.

Sandwiched between having to support our parents and our little boy, we prioritised their needs and finances were definitely a struggle. Everything costs money!

We didn’t have government schemes like the Baby Bonus or MediSave top-ups for newborns to help us in those days. So, we had to bite the bullet to set aside 10% of our monthly salaries for our kid’s future in savings and fixed deposit accounts.

Done with relying on children as retirement plans

We were thankful when we started earning more as we advanced in our careers. That helped to ease the edge on our finances, especially right around the time when my father retired.

But going through that experience made us realise that we didn’t want to place the same pressure on our own children. We didn’t want to feel like a burden to them as they would have their own families to worry about. Not to forget, cost of living continues to increase.

As a couple, we shared the mindset of wanting to be self-sufficient in our golden years.

Made a plan for ourselves and our children, with small and steady adjustments

However, creating this plan didn’t cross our minds until one day when Janet was asked to retire from her job. She got a little worried and we had to talk about what we wanted to do, what we could afford, and lifestyle adjustments we had to make.

We decided that we had to give up certain things and live a little more frugally. For example, we still take holidays to destinations around the region, but reserve longer holidays far from home for more special occasions — this also gives us a change to steadily save up for the longer holiday.

It was also at that point when we realised we hadn’t really considered what we wanted for our future selves after we retired, especially to occupy the time when our children would have become independent and didn’t need our care.

Our approach was simple—money makes the world go round. With money, we’ll be able to do whatever we want to do, particularly in retirement when we have even more free time on our hands.

So the most straightforward thing to do was to accumulate even more, right?

But we hadn’t always made all the right decisions with our finances.

At one time, when it was announced that you could use the savings from your CPF to invest in stocks and shares, we did, but some of them didn’t do so well. It would have been better to keep the money in our CPF accounts where they would earn risk-free interest. Thankfully, we didn’t take big risks and didn’t incur huge losses.

We had no luck with growing our wealth through investments, yet now we’re lucky to still be able to pursue our personal passions, despite not doing anything special to plan for retirement.

Following the flow, with CPF

Right now, we’re not working for the money, but truly taking the time to explore our interests.

We have our CPF savings to give us monthly payouts so we are less worried about paying for day-to-day expenses.

When we were younger, we did feel the pinch when it came to contributing to CPF, and the different schemes didn’t matter much to us at the time when were in our 30’s and 40’s.

It was only when we reached our 50s that we became more aware of how CPF was going to help us and we can appreciate how beneficial it has been to us through our lives.

Our CPF working contributions had been compounding steadily at interest rates of up to 5-6% per annum to finally give us these monthly payouts, which have been quite sufficient to last us through each month.

Still going with the flow, but with more options

We do believe that if you work, contribute to your CPF accounts1 and make prudent choices, you should have enough to see you through retirement comfortably.

But if we had had our serious conversation earlier on, we would have planned to save quite a bit more.

It’s still not too late. We have started making cash top-ups to our CPF, so that our savings can earn the attractive interest, and we can receive more payouts.

I’m just grateful for the options we have, and we’re content with our lives right now — being fit and mobile to do what we love.

Janet had the option of continuing to work part-time but decided to go back to her first love: baking. She used part of her SkillsFuture credits to learn about bread making and took a basic hygiene course. I’ve been exploring courses in social media, e-commerce, and video production. Last year, I went through a Professional Conversion Programme (Specialist Diploma in International Trading). I enjoy working because it keeps me moving; I meet people, and I never stop learning.

I’m also in a worship band for church and we play almost every week. In fact, at the end of this year, there’s a music festival and our band has been selected to perform.

It’s good to have different things to look forward to.

Take small and steady steps to build a purposeful retirement

My humble advice to you — coming from someone who has been there, done that, and is still doing it — is to think about your purpose and your life after work sooner, rather than later. That will give you a longer runway to start saving for whatever it is you’d love to do.

And your plan must be flexible to adjustments to make full use of the opportunities or options that come your way.

We’re currently not on CPF LIFE but we understand that it provides monthly payouts for life, no matter how long you live. That is something worth considering to ensure we don’t run out of our retirement savings.

We’re also thinking of taking up the Lease Buyback Scheme (LBS). Both of our children have moved out, but we’re quite fond of our home — Janet needs the spacious kitchen for her baking! Money-wise, it doesn’t make sense for us to try to sell and buy a new home. We did the calculations, and we’ll have quite a comfortable income with the LBS, on top of our CPF payouts.

When it comes to healthcare expenses, we have our MediSave savings to fall back on should anything happen, which also pays for our critical illness policies, on top of MediShield Life — an insurance every Singaporean has that covers pre-existing conditions. We may also consider upgrading our ElderShield to CareShield Life, simply because the latter would cover severe disability for life too.

Janet and I will have to do our sums and weigh the options again.

For nearer next steps, we’re also thinking of cutting back. Our daughter suggested that we give up the car, which could save us up to $1,000 a month. She pointed out that because we don’t go out as much, the car is parked more than it’s driven!

I think it’s important for both generations to be open with each other about finances, and to communicate so that we don’t have to worry about each other.

Along the years, we’ve realised that we’ve had more and more options that helped us to determine what kind of retirement lifestyle we want.

With the range of options out there, you no longer need to rely on luck alone, like we initially did!

1In 2020, 64% of active members were able to meet the Full Retirement Sum (FRS) in cash, or have meet the Basic Retirement Sum (BRS) and owned a property. An active CPF member is a person with at least one CPF contribution paid for the current or any of the preceding three months. Correspondingly, the attainment rates are lower among all members at 51%, as this includes those who are economically inactive or not in regular employment before age 55 and thus not able to accumulate CPF savings consistently.

Cedric de Souza is a retired advertising veteran, currently working as an education consultant. His wife, Janet Tay, used to be a bank officer and now runs her own home bakery from the couple’s flat in Pasir Ris.

Information in this article is accurate as at the date of publication.