2 June 2022

SOURCE: DollarsAndSense

With homeownership rate in Singapore at about 89% as of 2021, your homes are naturally part of your retirement plans. For homeowners in Singapore, owning a home implies not having to worry about paying rent during your retirement. If you want to, you can even monetise your home to increase your passive income during retirement.

In this article, we will discuss some of the common options for HDB flat owners to monetise your flat for retirement needs.

You may prefer to move in with your children or move to another flat that better meets your needs. Either way, you can consider monetisation options to unlock the value of your flat to boost your retirement savings.

Firstly, if you have alternative accommodation, you may choose to rent out the entire flat. This would allow you to earn rental income that can be used to fund your retirement.

Otherwise, you may choose to sell your flat. If you sell your current flat or private housing with an annual value not exceeding $13,000 and buy a 3-room or smaller flat, you may also qualify for the Silver Housing Bonus (SHB) of up to $30,000. To qualify for this, at least one owner must be a Singapore Citizen aged 55 and above, and you will be required to top up $60,000 of the proceeds in your CPF Retirement Account and join CPF LIFE. If the top-up is less than $60,000, you will receive a pro-rated cash bonus based on a 1:2 ratio, i.e. $1 cash bonus for every top-up of $2.

Some of you might wish to move near your children, for practical reasons. This makes it convenient to plan family gatherings, help look after your grandchildren, and provide or receive support, if a family member is ill.

If you intend to purchase an HDB BTO flat within 4km of where your child is living, you can consider applying for the Married Child Priority Scheme (MCPS) or the Senior Priority Scheme (SPS). You may also consider applying for flats together with your married child in the same project via the Multi-Generation Priority Scheme (MGPS) – this allows you and your married child to select flats at the same time within the same BTO project.

Alternatively, you may purchase an HDB resale flat and apply for the Proximity Housing Grant (PHG) of $20,000, if you buy a resale flat within 4km of your child’s residence.

Read Also: Guide To Understanding The HDB Proximity Housing Grant (PHG)

With all these support, it means right-sizing to a home that better meets your needs comes with financial benefits.

For example, if you currently live in a 5-room flat in Punggol (median HDB resale price $600,000, 1Q2022) and are intending to move to a 3-room resale flat at Bedok (median HDB resale price $335,000, 1Q2022), the price difference would be $265,000. This assumes that we use the median HDB resale price as of Q1 2022 as a reference, and without taking into consideration the PHG.

Even if we add in transaction costs (agent commission, legal fee, Buyer Stamp Duty) and a renovation budget, you could still retain about $200,000 if you move from a 5-room flat at Punggol to a 3-room resale flat at Bedok.

With the proceeds from the right-sizing of home, you can meet the Full Retirement Sum of $192,000 (for members turning 55 in 2022), giving you a lifelong monthly payout of between $1,450 - $1,550 from CPF LIFE. Of course, you can also choose to top up your Retirement Account to the Enhanced Retirement Sum ($288,000 as of 2022) if you want a higher monthly payout. If you top up at least $60,000 of the proceeds into your CPF, you would receive a cash bonus of $30,000.

While some may elect to right-size your home once you no longer need the space, there are others who may feel sentimental and have no desire to live elsewhere. Even then, you can still monetise your existing flat by renting out a spare bedroom in your flat.

You may also opt for the Lease Buyback Scheme (LBS). The LBS allows you to sell part of your flat’s lease to HDB and receive a stream of income in your retirement years, while continuing to live in your flat.

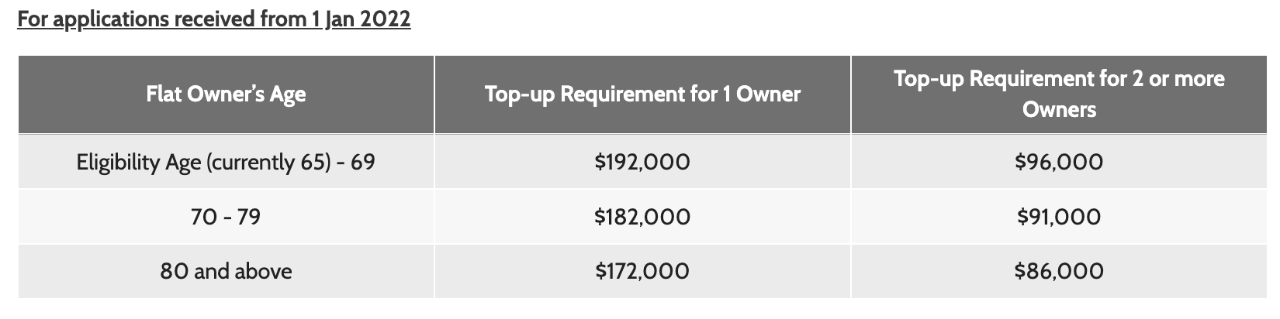

For example, if you are both aged 65 and currently living in a 5-room HDB flat that you co-own with a remaining lease of 70 years, you can choose to retain 30 or 35 years of the lease.

By selling part of your flat’s lease to HDB and using the proceeds to top up your CPF Retirement Account to the specified requirement shown below, you will receive higher CPF LIFE payouts and an LBS bonus in cash (up to $30,000 per household depending on the flat type and top-up amount). Do note that the retained lease needs to cover the youngest homeowner up till the age of at least 95.

Based on the figures in the table above, the CPF top-up requirement is $96,000 per individual. If we assume that you each have $30,000 in the RA today, the top-up to your RA would be $66,000 per person, or $132,000 in total. This amount will come from the proceeds you get from selling the lease to HDB.

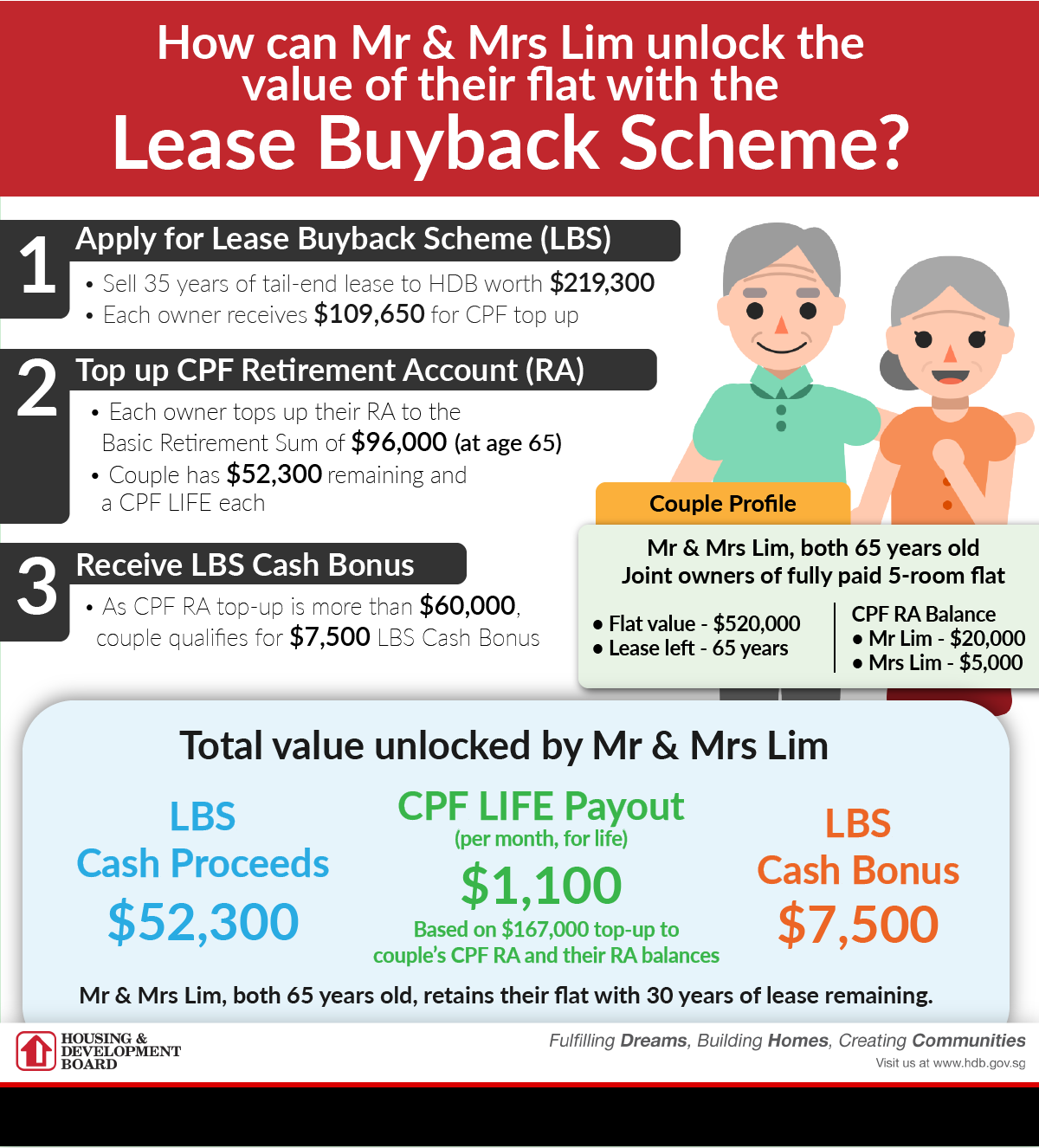

Here’s an example from the HDB website on how the Lease Buyback Scheme would work. This is based on a 5-room flat.

There are 3 main advantages with the Lease Buyback Scheme.

Firstly, there is no need to move out of your home. In fact, you can continue living in your home for the rest of your life.

Secondly, selling part of the remaining lease will allow you to receive proceeds from HDB that can be used to top up your CPF RA, thus increasing your monthly CPF LIFE payouts in your retirement years. You also receive any excess proceeds in cash.

Lastly, you will receive an LBS cash bonus of up to $30,000, depending on your flat size and the amount of CPF top-ups made.

Read Also: HDB Lease Buyback Scheme Now Open To All Flats: Here’s How It Works

All the options that we have highlighted are possibilities that you can consider if you wish to monetise your HDB flats to increase your passive income during retirement. However, your choice will ultimately depend on your personal preferences and family circumstances.

For those who are living with your adult children, perhaps for health reasons or otherwise, renting out the entire flat (or even selling it) could be a viable option. The amount received can be used to help supplement your retirement.

For those who prefer to age in place, you could choose to rent out a spare bedroom. You can also choose to take up the Lease Buyback Scheme, which allows you to enjoy more retirement payouts via CPF LIFE when you top up your Retirement Account.

Finally, for those wish to move into a home that better meets your needs, moving to a smaller flat and potentially utilising the Silver Housing Bonus could be a desired option.

This article was written in collaboration with the CPF Board. All views expressed in this article are the independent opinion of DollarsAndSense.sg based on our research. DollarsAndSense.sg is not liable for any financial losses that may arise from any transactions and readers are encouraged to do their own due diligence. You can view our full editorial policy here.

Information is accurate as of the date of publication.