14 Feb 2023

SOURCE: CPF Board

Planning for a new home is the ultimate romantic gesture - it lasts longer than flowers and gifts, and is a commitment to each other and a shared investment for your future together.

This is why it’s important to approach the journey with care and consideration to ensure you’re both on the same page and ready for the responsibilities that come with owning a home together. Here are some questions to help you find the One – the ideal and affordable house for you and your partner.

The starting point is to identify what kind of home best suit your needs.

Build-to-order (BTO) flats – newly built public housing units that are offered for sale through HDB. BTO projects are released periodically, and they come with a fresh 99-year lease.

Resale flats – pre-owned public housing units that are sold by current flat-owners. Resale flats offer the advantage of a relatively shorter waiting time compared to BTO flats, as they can be readily available and open for occupancy in a short space of time. However, they are typically more expensive than BTO flats due to factors such as market demand and location.

Rental – if you need a temporary place for short-term needs or if you just want to experience living with your partner, you can also consider renting a place. But unlike the first two options, you can’t use your CPF to pay for your rent, meaning that you have to fork out your hard-earned cash.

Rental prices in Singapore surged last year, with prices for private housing rising by nearly 30 per cent, the biggest jump since 2007. If you have decided to rent, make sure you evaluate your expenditure in the long run, especially when you do not have the option of selling your property.

When choosing between your housing options, think about factors such as budget, timeline, personal preferences as well as the overall market conditions so that you and your partner can make an informed decision.

You'll probably have that ideal location for your dream home in mind. Shortlist your preferred locations– but do balance your dream against the practical aspect of affordability.

Flats in mature estates tend to be more expensive than the ones in non-mature estates. If your concern is non-mature estates might not have sufficient facilities, the rapid growth of Singapore’s infrastructure – development of regional hubs, heartland amenities and expansion of the MRT network – will alleviate that concern as this could also be a longer-term benefit.

A factor that should weigh in your thinking is the proximity to your family members. Outside of the obvious benefits of being close to your loved ones, you can also enjoy housing grants and priority schemes if you choose to stay near your family.

There are different factors to consider when it comes to financing your home.

Tapping on CPF savings, as well as various housing grants and schemes

You may also be eligible for a number of additional housing grants, depending on your flat/household type and their respective eligibility conditions.

Decide on how you are going to pay for your mortgage

Not all of us may have the luxury of paying for our home upfront, so a housing purchase has potential long-term ramifications. One key decision to consider is what type of loan you want to take – either a HDB loan or a bank loan.

As a potential first-time homebuyer in Singapore, you may be affected by the impact of rising mortgage rates. Banks in Singapore have been gradually removing their fixed-rate home loan packages and offering ones that are pegged to the Singapore Overnight Rate Average (SORA).

The 3-month compounded SORA has been steadily increasing over the past year and as a result you are likely to see higher average interest rates in the coming months. For reference, the current three-month Singapore Overnight Rate Average (SORA) is at 3.19% as compared to 1-month SORA rate of 3.58%*.

*Information taken from MAS website on 6 Feb 2023

This means that you may see higher monthly instalments for your home loan over time. Therefore, it is imperative to exercise extra prudence when borrowing and to maintain an emergency fund to provide you with a safety net when there is less certainty in the current interest rate environment.

So, does this mean that you should go for a HDB loan? Not necessarily, as there are many factors to consider. It all depends on your specifics needs and preferences.

Here are the key differences between a bank and HDB housing loan:

Bank loan |

HDB housing loan |

|

Loan quantum |

|

|

Downpayment and payment during key collection |

|

|

Use of CPF savings and previous property sales proceeds |

|

|

Interest rates |

|

|

Repayment amounts |

|

|

Capital repayment or refinance loan |

|

|

A good starting point would be to ensure the house is within your means through the use of housing ratios. A housing ratio shows us how much of our income is spent on housing. Use these two housing ratios to keep your housing budget in check:

Mortgage Servicing Ratio (MSR) - refers to the portion of a borrower’s gross monthly income that goes towards repaying all property loans, including the loan being applied for.

A maximum of 30% of your gross monthly income should be used for your monthly loan repayment. To be prudent, keep it within 25% to give you more room for other financial commitments.

Total Debt Servicing Ratio (TDSR) - refers to the maximum proportion of an individual’s gross monthly income that can go towards repaying all monthly debt obligations, including the loan being applied for.

The current TDSR threshold is set as a maximum of 55% of the borrower’s monthly income.

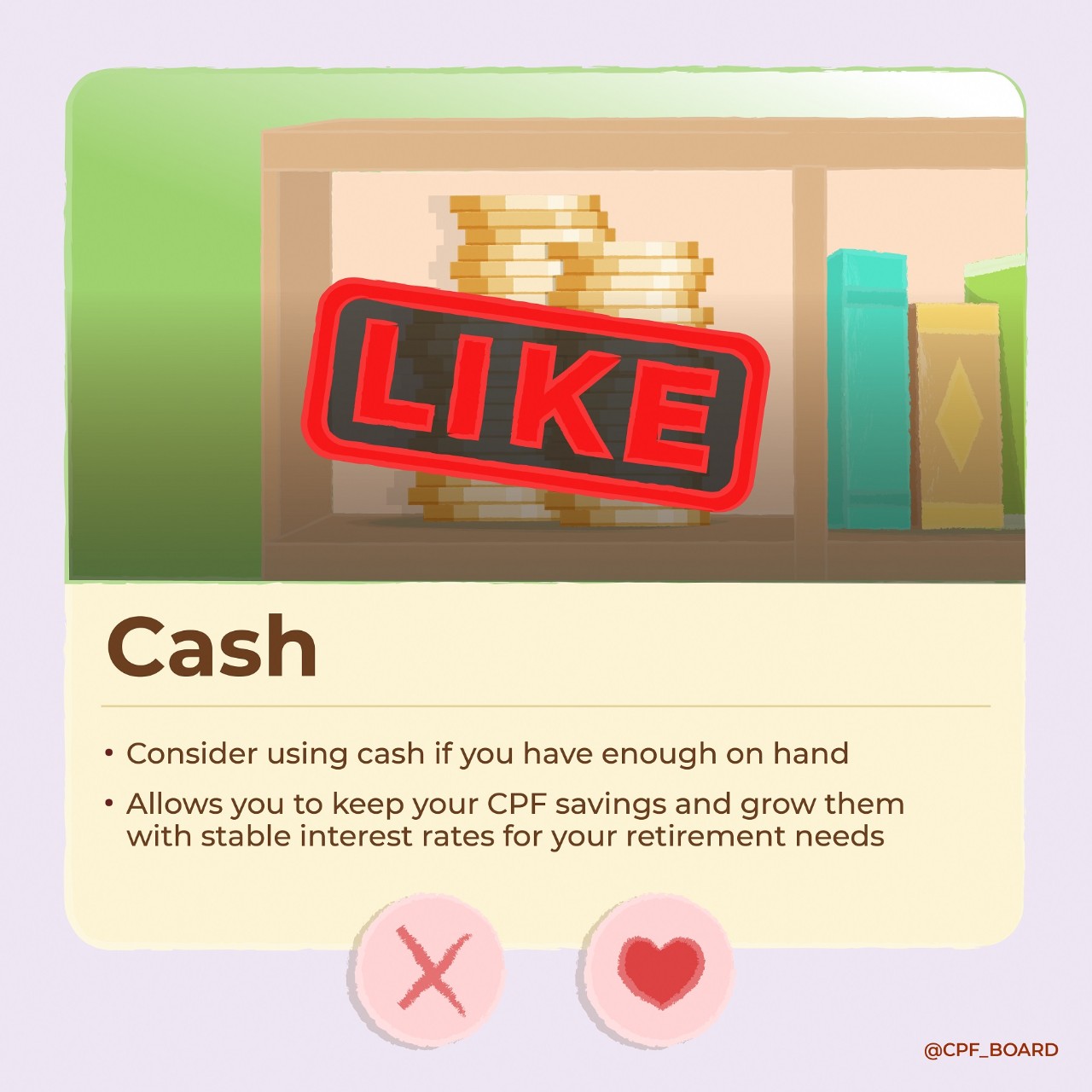

Using Ordinary Account (OA) savings/cash

Most people consider the money in their OA as the primary source of funding for their home purchase, but it’s vital to weigh its impact on both your present and future financial goals. While your CPF savings is a valuable tool for home financing, it also serves as your retirement income in the future.

Note: There are other expenses that can only be paid with cash, for example property tax, application/option fees and fire insurance.

Once you have your home – what’s next?

It may be tempting to splurge to build your dream house. But it's important to note that renovation costs might be quite hefty, and can even go up to 6 figures!

Consider if you need to engage an interior designer, especially if you don’t need help to conceptualise the aesthetics of your home or project manage your home renovation. If you are comfortable being more hands-on, you can go directly to a contractor to execute the plans you have in mind. That can allow you to save more.

Other tips to build your new home:

Plan ahead – clearly define your renovation goals and budget, to avoid overspending during the process

Prioritise – focus on essential upgrades/items that add value to your home

Do-it-yourself – Take on tasks that you’re comfortable with, such as painting the walls

Shop around – Compare prices for materials and wait to get discounted big ticket items during sales

Reuse and recycle – Salvage and reuse materials such as cabinets and appliances where possible

Go green – Buy and install energy-efficient appliances and upgrades to help you save money in the long run

Learn how 3 homeowners used their CPF to budget for their home and renovations

In a way, buying a home is like falling in love. You begin casually by looking around and exploring options, before getting serious and figuring out what matters to you. Then as things get serious, you plan towards achieving your desired outcome – a happy ever after.

By asking yourselves the questions above, you and your partner can define your relationship with less drama. Remember to approach the process with care and caution, and be open and honest with each other to ensure a smooth and successful home ownership experience.

Because it’s not just finding a place to call home, it’s also about making a wise investment that will shape your future.

Information accurate as of date of publication.