12 Jun 2026

SOURCE: CPF Board

Buying your first HDB flat, is a big milestone, and one of the biggest decisions you’ll have to make is how to finance it. Should you choose an HDB loan or a bank loan? From housing loan interest rates to HDB downpayment requirements, the two options differ in ways that could shape your cash flow and long-term financial plans.

Here are three key differences to consider before making your choice.

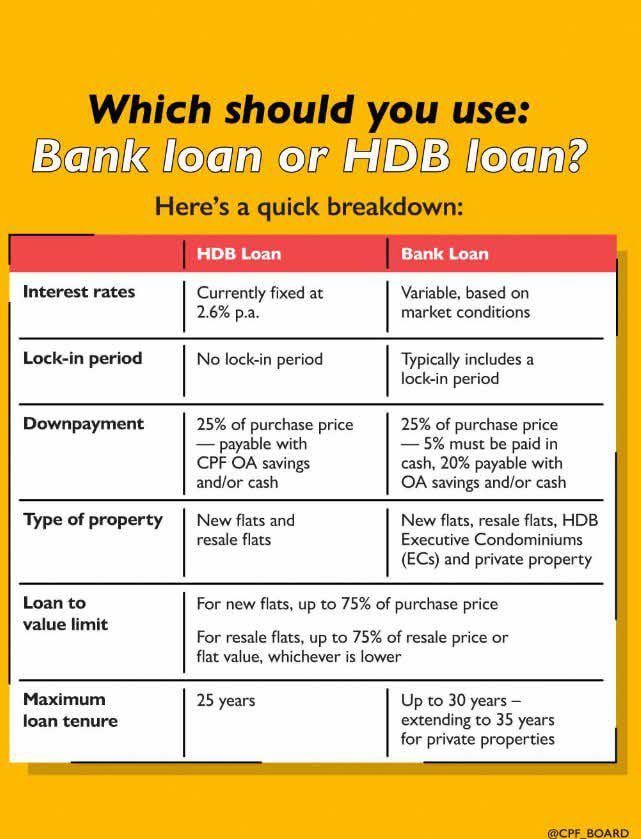

1. What to know about the housing loan interest rates

Interest rates directly affect your monthly mortgage payments.

HDB loan:

The HDB loan interest rate offers a concessionary interest rate, currently fixed at 2.6% per annum and is pegged to the CPF Ordinary Account interest rate. This fixed rate provides stability and predictability for your monthly repayments.

Bank loan:

In contrast, bank housing loans offer floating interest rates pegged to a benchmark such as the Singapore Overnight Rate Average (SORA) or fixed interest rates for a pre-determined time period (usually one to three years) before reverting to floating. These rates are subject to market fluctuations.

2. Comparing downpayment requirements and using CPF

HDB loan:

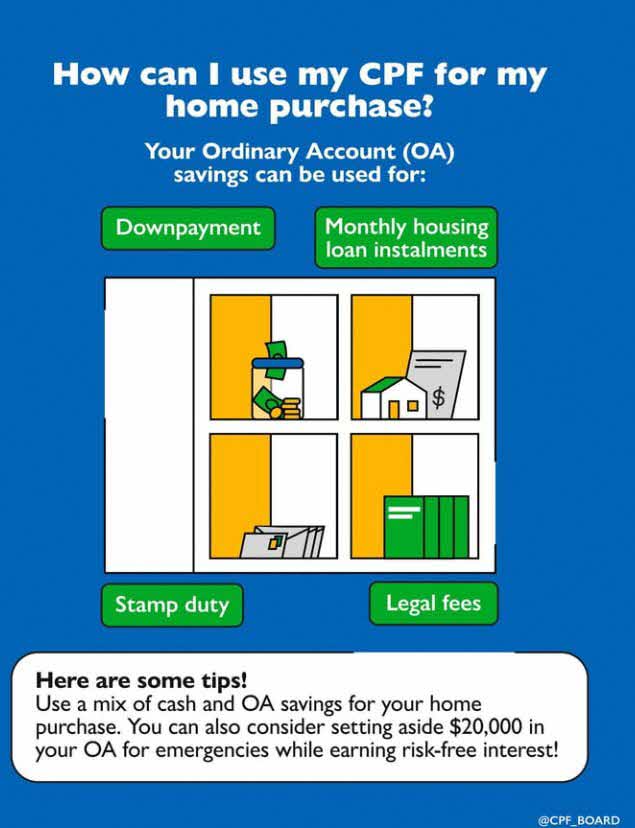

- Downpayment: At least 25% of the purchase price, which can be paid in full using your CPF Ordinary Account (OA), with cash, or a combination of both.

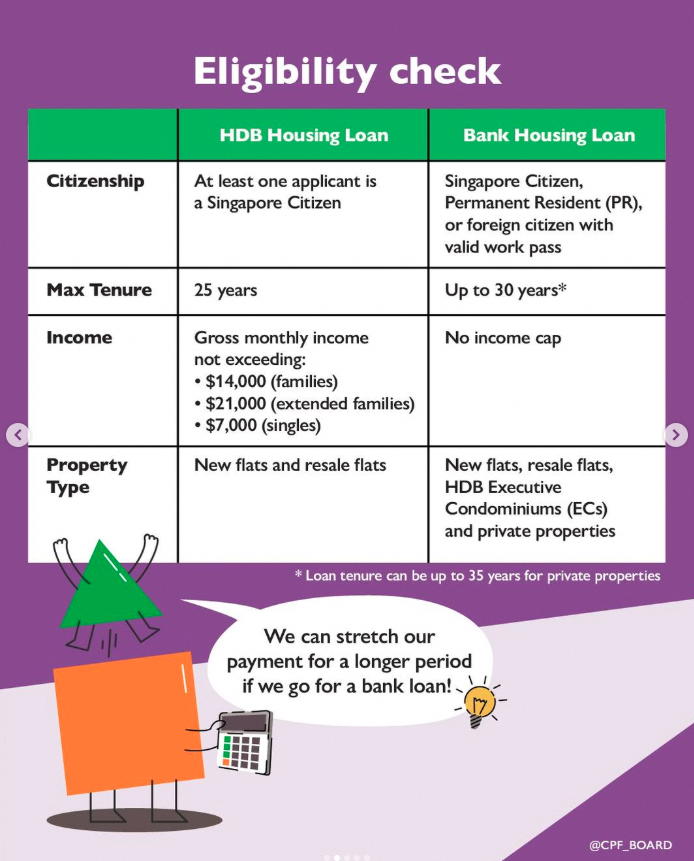

- Maximum loan amount: Up to 75% the purchase price for BTO flats. For resale flats, it is 75% of the resale price or market valuation (whichever is lower). This amount will also depend on the Mortgage Service Ratio (MSR), which means that your monthly housing loan repayments cannot exceed 30% of your gross monthly income.

Bank loan:

- Downpayment: 25% of the purchase price, with 5% payable in cash and the remaining 20% payable in cash or your CPF OA savings.

- Maximum loan amount: Up to 75% of bank valuation or purchase price (whichever is lower). Keep in mind that bank loans are subjected to both the MSR and the Total Debt Servicing Ratio (TDSR) limits, meaning your total monthly debt obligations cannot exceed 55% of your gross monthly income.

For BTO flats, the downpayment applies at the point of key collection, giving you more time to build up their CPF savings. For resale flats, the downpayment is required at the point of purchase, which means you need to have your funds ready sooner. If the resale price exceeds the market valuation, the difference, known as the Cash Over Valuation (COV), must be paid fully in cash and cannot be covered by CPF or your loan. Therefore, if you opt for a bank loan, there is a risk of needing to pay both the 5% downpayment and the full COV amount in cash.

3. Lock-in period - do you prefer stability or flexibility?

Many homeowners review their mortgage repayment every few years.

HDB loan:

There is no lock-in period, so there will be no penalty if you wish to pay off your loan early. This also means that you have the option to refinance your loan with a bank anytime.

Bank loan:

Most bank loans on the other hand have a lock-in period, typically around one to three years. If you would like to pay off your loan early or refinance your housing loan with another bank within the lock-in period, you will incur a penalty. That could be around 1.5% of the outstanding loan amount, although terms vary based on the bank and loan package. It is also worth factoring in other refinancing costs such as legal fees, valuation fees, and potential clawbacks of subsidies or rebates from your initial bank.

So, which loan are you eligible for?

When it comes to choosing between an HDB loan and a bank loan, it is essential to carefully consider your financial situation, risk tolerance, and long-term plans. Most of us focus on getting the keys to our dream home and forget to think about what it means for our retirement. But the two are more connected than you think, and your financial circumstances can change over time.

That's where the CPF Home Purchase Planner comes in. It’s the easiest way to keep track of how changes in your finances or housing situation could affect your housing budget and future retirement. It also offers you a more personalised look at how you can balance the use of CPF for housing and retirement, so make it a habit to review it regularly and plan for both with confidence.

The information provided in this article is accurate as of the date of publication.