About 800,000 home owners use CPF to pay their housing loan instalments each year

8 in 10 home owners aged 50 and below who used CPF to pay their loan had sufficient CPF savings for at least 6 months of instalments

No. of home owners using CPF for housing loan instalments in Dec 2023

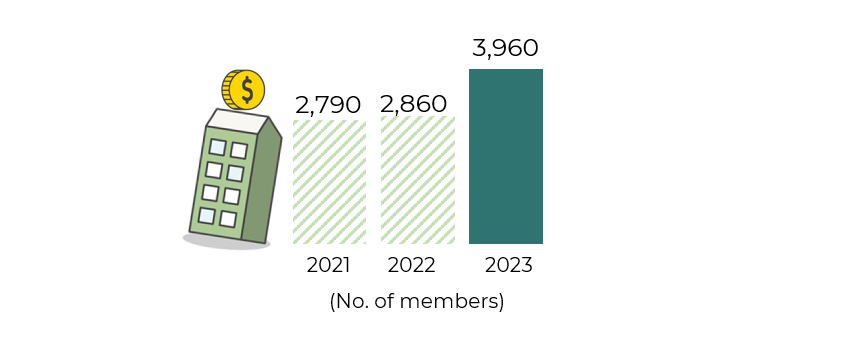

15k members made voluntary housing refunds in 2023

Notes:

- The higher interest rate environment for 2023 had made financial instruments more attractive than the Ordinary Account interest rate, which may have resulted in fewer members making voluntary housing refunds in 2023.

Owners for over 9 in 10 properties fully refunded CPF used when they sold their property

Notes:

- Figures refer to properties sold within the year

Increase in take-up rate of Lease Buyback Scheme and Silver Housing Bonus

Total amount received in cash and CPF by members from the Lease Buyback Scheme and Silver Housing Bonus has increased

Resources

Need more information?